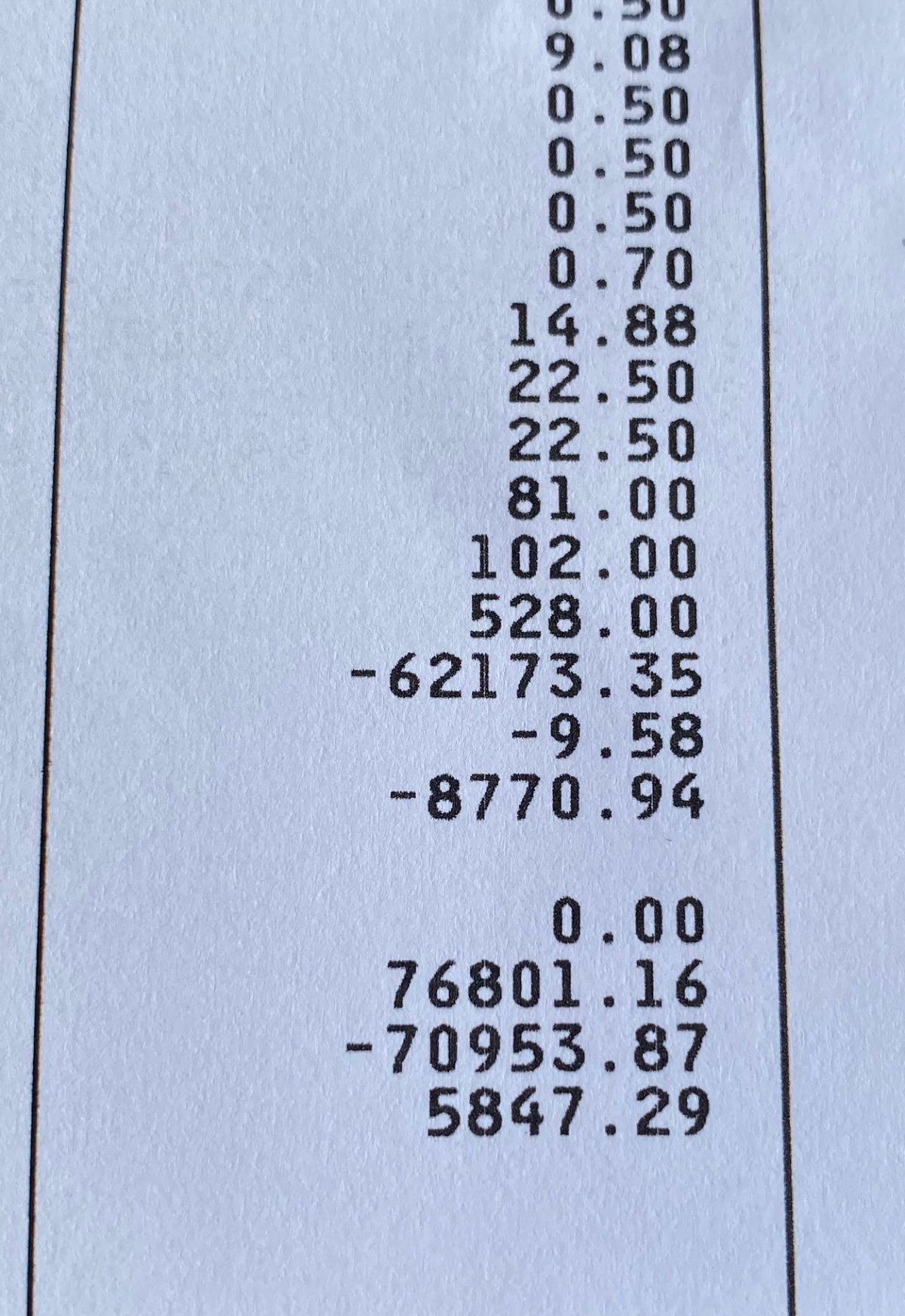

I got a frightening lesson in the awful state of American health care yesterday when I came home from doing chores to find a bill from the Albany Medical Center, one of the most respected hospitals in the country, for $5,487.29.

I expected and was told that my operation – a catheter procedure on a blocked artery to my heart – had been pre-approved by my insurance company and had no indication there would be any additional charges from people not in my health plan coverage list.

I think the shock was as bad as the bill. And I think this kind of billing is wrong.

I had Open Heart Surgery six years ago and paid a $300 co-pay. I had a previous catheter procedure and paid a $180 co-pay. My latest operation cost $76,000.

This was a jarring thing to see, and I admit it got to me. And I should have been prepared.

Going online, I find that it also happens to one in three Americans every year, especially for emergency room or ambulance treatments (many ambulance services charge $300 a mile.) Hospital bills to unsuspecting people are staggering, and in my mind, scandalous.

What on earth is insurance for? Why should so many Americans need to launch gofundme campaigns for fellow citizens drowning in “surprise” medical bills?

I wanted to write about this to share the experience and warn people to be careful when they need medical care that involves a hospital or other emergency care facility.

I went on several medical websites to find out my options.

My bill was a simple list of costs, but there was no explanation for hardly any of them. I can’t imagine any layperson understanding any of it. And I suspect that’s just what they are counting on.

It seems unlikely that I will be able to spot any mistakes if I read over the list. But I will ask for one anyway.

I will call my doctors in the morning. They are helpful and available and will let me know if there is anything I can do. I will call the insurance company and ask them to review the costs and see if there were any mistakes made on their part.

And I will call the hospital to ask them to review the bill and the costs listed. If that all fails – and usually does- I will have to negotiate monthly payments with the hospital over time.

I know myself well enough to go I can’t deal with protracted fights with giant corporations and bureaucracies. And I doubt they are breaking any law.

Like most people, I don’t have anywhere near that much money in the bank, but I can and will repay a valid bill over time.

I am fortunate to be able to do that.

I am grateful for this heart procedure, it has made me stronger and healthier, and I consider it a matter of honor to pay my bills on time and by myself.

I am so grateful that no refugee family I work with has gotten a bill like that; I shudder to think what it would do to them.

There are so many stories worse than mine.

I understand that I am fortunate to have good insurance at all in America.

I know many people who refuse to see doctors or go to emergency rooms for this very reason. That is a national disgrace.

As a diabetic and someone with heart disease, I don’t have the option of avoiding health care. I suppose that is also true of the many people who feel they have no choice.

I don’t expect that this particular bill is a mistake since it has happens so often to so many people all over the country. I could lie and pretend I will fight it to the end, but I know myself better than that. Maybe it’s the Dyslexia, but I just don’t have a mind for arguing over figures and details.

Congress is considering banning the practice of surprise billing, but it is deadlocked about it as usual – too much lobbying money in the way.

This was a hard pill for me to swallow, for some reason, it just hit me hard. I didn’t sleep much last night.

Since our bankruptcy, when we couldn’t sell the first Bedlam Farm, I have worked hard and diligently to get our finances in order and rack up a spotless credit history.

Perhaps that’s why I was so sensitive to it.

I will deal with it, for sure, and be grateful for the fact that I can. And for my restored heart.

Since I was totally unprepared for this and no one at the hospital even suggested such a thing might happen, I realize now that there are many questions to be asked when undergoing hospital or emergency care.

I didn’t ask enough of them. If I can spare anyone from that mistake, that will be gratifying.

I would advise anyone who needs a hospital or emergency health to be aware of what the health care industry calls “balance billing,” better known as “surprise billing.”

This happens when a patient receives care from a doctor or hospital outside of their insurance network. Subsequently, the doctor or hospital bills the patient for the amount insurance didn’t cover.

“They add insult to injury,” says Forbes Magazine, “tormenting the American consumer of health care.”

This is true; I felt both insult and injury when I got this bill. I am fine, but it seems cruel to send a heart patient-days after recovering from a heart attack or someone coming off of chemotherapy to get an unexpected bill like this.

I’ve met people who had heart attacks over less. And this from institutions that are supposed to save us, not scare us to death. When I call the insurance company, I will ask them if it seems appropriate to try to give people heart attacks when they claim to be helping them instead.

That will get me nowhere. I might get lucky, either with the doctors or the insurance company itself. I won’t hold my breath.

Surprise bills are symptomatic of the very complex ways healthcare prices are set in the United States and no other country in the world. They are supposed to reflect the difference between in-and-out-of-network costs to the insurer.

They are based on the assumption – often quite false – that health plans contract with doctors, hospitals, and pharmacy networks to reduce the costs of care and keep premiums low for insurers. They save money for insurers but don’t reduce the costs of care for consumers.

When did you last see your premiums or co-pay fees go down when all of the care is within the network?

I started to blame myself for this, but Maria slapped me around, pointing out that I had no reason to expect anything like this.

I am big – perhaps too big – on taking responsibility for the things that happened to me, but she is right.

The hospital and the doctors did a wonderful job repairing my heart, and they deserve to be paid for it.

But this seems wrong to me, dubious and secretive and even cruel. Since I didn’t know much about it, I thought I should let others know about my bill. I am sure many of you do already.

I have both Medicare and supplemental insurance, and if I get hit with a bill like this, I can only imagine what happens to people with less coverage.

I gave everyone the right checks and credit cards, paid for whatever I was asked to pay, and no one even suggested this might happen.

I hope November leads us towards being a more caring, gentle, and loving country.

The US government and Big Pharma along with the corporate health insurance companies are fraudulently implying this is the way it is, “We are doing our best”. They are in it together, complicit thieves, when it is blatantly clear that universal health care is the only way that equal health care for all can be obtained. I live in Canada and that surgery along with anything else is covered in it’s entirety. Canada is not the only civilized nation to have it, we are one of many…all except the US. It’s outrageous and evil.

John… you can dispute such a bill. You are only responsible for the in network cost copay. See attached.

https://www.dfs.ny.gov/IDR

Wow. My heart leapt in my chest when I read this. Why didn’t anyone alert you to this PRIOR to your procedure? How is one to know?

Yes. Exactly.

What can one do prior to the procedure to prevent this?

Call me cynical but I’d be very surprised if you don’t receive enough and more to cover this bill.

You’re cynical..This is my fourth procedure and I’ve never gotten a surprise bill like this..It’s not inevitable and I’m sure I will have to pay the bill..

This is a good readon to have traditioal medicare, plus a supplental. It costs more, but there are no networks. I’ve had major surgeries with no big bills…no surprises. I’d advise you to switch. This is why I don’t have medicare advantage.

I used to work in managed care, and even though I have an understanding how the system works it still remains opaque and complicated. Many of the rules insurers use to pay or not pay are obscure and well hidden from the covered person. Not stated in any certificate of coverage. Everyone needs to be an aggressive investigator, persistent and pushy, asking the right questions and not settling for vague answers. You need to know all the ways you can get stuck, which is hard. Online research might help. I will say the situation is far worse fir commercial ( group and individual) insurance than with Medicare. Medicare rules, both for traditional and Medicare Advantage, prevent balance billing. I’d suggest beginning with the assumption that everything should have been covered and inquire as to why it wasn’t. If some loophole occurred in the healthcare system, such as using a non-Medicare provider for part of your care, so they are not bound by the Medicare rules, file a complaint with CMS or the Medicare Advantage plan and CMS.

That is the state of health care and insurance in this country. Almost unique in the developed world. Non-Medicare families pay thousands in premiums, pay thousands more for deductibles and cost share, and still find they are on the hook for thousands that were unexpected and often unfair.

I would strongly recommend giving a listen to the podcast An Arm And A Leg, or at least check out the website https://armandalegshow.com

It deals with exactly this sort of thing and offers some suggestions.

Did you check if the bill was submitted to your supplemental insurance? This happened to me once. The hospital submitted the charges to Medicare, and although the supplement was listed in my records, billing “forgot” to submit it to the supplement.

I’ve been living in France for the past 20 or so years. My brother is a doctor in the U.S. The last time I visited, he asked me how it is living in a ‘Socialist’ country (he’s a Republican, and I imagine that he watches his share of Fox News). The next time that he asks me this question, I’m going to send him a link to your story.

The AARP had an article about which countries were best for Americans to retire in.

France was rated as having best healthcare.

The other half of the insanity is what insurance companies exclude from your deductible, especially insulting with “high-deductible’ plans. You get a bill from a doctor or a medical institution. You pay it, and then you get a statement from the insurance company that says they’re only going to count 10% of what you paid towards your deductible. It doesn’t matter that you paid it they don’t care.

As far as I can tell, there very little health or care in our healthcare system, something I hope changes if our congress is able to function again.

Definitely ask for an explanation here. Nicely, but firmly. The hospital and, I assume, your surgeon, knew (because of your age) that you were on Medicare. If anyone (anesthesiologist, other) did not accept the Medicare assignment for their services, you should have been notified in advance for what was elective surgery. And even so, there is by law what is called a “limiting charge” that restricts billing by someone who did not accept the Medicare assignment to no more than 15% more than the Medicare-approved cost for the service. But it’s hard to believe that any medical provider or hospital involved in providing cardiac care didn’t accept the Medicare assignment. Probably 90% of their cardiac patients are on Medicare.

Your supplemental insurance is not good enough! I pay 625$ a quarter with Blue Cross and never got a bill for anything and I have had many operations since I turned 65

First call your insurance company.

Don’t negotiate anything until you do.

M.

Yes make sure you give the insurer a chance to correct any errors before you approach your doctor. Some doctor’s have a point person who understand the complexities of how your insurer works and can help. They also have social workers who can often help.

Don’t panic. My husband had the same procedure done at the Mayo in Rochester, MN and also received a large bill. After calling everyone involved we were told to wait. Don’t pay the bill and see if Medicare or our supplemental insurance would cover more. They did and after three months all of the bill was covered. Hopefully, the same will be true for you. Sometimes it’s just a coding err that causes the bill to not be paid by the insurance company.

You are going down the right path. Request an itemized statement for the bill. Check every item. Hospitals charge for items ordered for whether you use them or not. An example, my two-year-old son was hospitalized for asthma. I stayed with him the whole time and provided all his care. When I received the bill, there was a charge for 300 for urinary analysis. I asked when and how they did it. They said they had probably attacked a device to his penis,; I knew it did not happen. The cost was deducted. My husband had thyroid surgery and a “storm tray” was ordered and delivered. The cost was 500. He did not use the tray and i insisted that it be deducted from the bill. Your bill may not be this easy to correct, but it will be worth the try.

I have been dealing with my husband’s heart bills for years. I certainly understand your surprise and trepidation. I never pay a bill until I get the Medicare benefit statement, the supplemental insurance statement, and an itemized bill from the provider with both insurance payments deducted. I have also negotiated lower amounts. It can be a pain, but don’t give up.

This would upset me too. I once told my pharmacist I was having a heart attack. I was only half kidding. Coming from the neurologist I had a prescription for MS injections. I had been diagnosed that day. This was years ago. The pharmacist told me the medicine would cost $3,500 monthly. My friend was paying $80,000 for her monthly MS infusion treatment. Her insurance only covered 80% of the bill. I never did go on any medication for my MS which is okay. I have a progressive type of MS and should not be on medication anyway. I have Medicare and a supplemental plan too and I’m scheduled to have surgery in a couple of months so this blog was helpful. I’ll be checking everything out before I agree to the surgery. Thank you.

Thank God I live in Canada. We don’t receive bills of any sort for medical care. I have no idea what various operations cost because I never see an invoice. It’s a travesty that a country as advanced as the U.S. doesn’t see fit to provide universal health care. I’ve heard that lots of American politicians refer to the Canadian system as “socialized medicine”. The problem is that most people hear the word “socialized” and assume that it’s the same as the communist system, which couldn’t be further from the truth. Our system is far from perfect, but nobody has to choose between groceries and health care and nobody ever has to declare bankruptcy because they needed surgery.

I also have received bills like this following a hospitalization. I found that it pays to wait for your medicare statement. It will list all the charges that have been submitted , tells you if the bill is allowed, and how much Medicare allows to be charged, how much they pay. Then you can check your supplemental insurance to confirm they picked up their part. If the bill wasn’t submitted to Medicare, I insisted that it be submitted and waited for Medicare’s determination. I found that the bills I had received weren’t allowed and I did not need to pay them. Great news for me. I hope it works out that way for you as well.

Frankly, with the way insurance generally works, you’re lucky they paid as much as they did. What you had is considered an elective surgery: it makes your life better, but you could have chosen not to have it and not statistically endangered your life: that’s why your surgeon gave you a choice. Paying $5,000 on a $76,000 elective surgery bill is pretty good, all things considered.

Actually, Steve, that’s a bit too flip for me. I am lucky in many ways, as I said. That doesn’t mean this system is good or fair. I know too many people with chronic diseases who are terrified to go to the doctor at all for fear of bills like this, which they are not going to be able to pay..I think you’re blowing this off a bit too casually..I’ll be fine a lot of people won’t…I could have refused every heart procedure I have had..there were no surprises..

I am very sorry for the shock of this. I have a little experience as I used to work in the health care field that might be of benefit. First, when it comes to ambulance bills – just as an example – I got a surprise bill after going by ambulance to the ER about 2 miles from home. I followed up by contacting the ambulance company and found out that they didn’t have my insurance info. I was sure they asked for it. The outcome was I gave them the info Medicare and a Supplemental like you) and it was taken care of. I never heard from them again. Had I not called I would have paid up like so many senior citizens do.

You want to make sure that your secondary insurance has been billed and they paid. That’s another common source of a surprise bill.

And finally, most hospitals have the ability to cut the costs considerably if you don’t have a lot of income.

Ask for alternative sources of payment (they have special funds) and for a payment plan.

I hope this turns out much better than it appears right now. And hope something I have said turns out to be helpful. P.S. Medicare does cover ambulances.

I was in 3 different hospitals for 55 days (yes Covid and Rehab). It has been 5 months and I am still getting bills. Lab work. Radiology, Dr out off network and it goes on. Up to about $2500.00. Not looking forward to ambulance charges.

You should try to negotiate the price down. That is a common practice.

You can also ask about financial aid. I did that after I received a bill from the hospital the was basically owned by my insurance company for the ER doctor. I felt they should know that the doctor practicing at their hospital was out of network and why wasn’t he covered. I got hit with the ER copay and his 1000$ bill.

I now have a Medicare insurance supplement that allows me to go to any provider.

Jon…Every case I am sure is different but who is your supplemental carrier? I have been in the hospital many times and our Blue Cross after Medicare, has picked up everything. Have never paid one penny to the hospital. It is not cheap but certainly cheaper than a huge hospital bill.

Jon…

You have received a downpouring of good advice. Some is on target, but some seems confusing.

So let me suggest this first step as a certified counselor for the government-funded State Health Insurance Assistance Program (SHIP):

This might not be a surprise billing situation. The small amounts listed suggest this might not be a bill from an ancillary physician. A hopeful possibility is that your hospital’s billing department did not recognize that you had Medicare Supplement coverage. (This has happened to me.) Or that your supplemental carrier isn’t set up to accept automated claim data feeds from Medicare.

In those cases, the provider would have billed you for copayments. To rectify that, simply ask the hospital to forward the balance due to your supplemental carrier. If they resist, you might need to submit the claim yourself.

That said, surprise billings are a serious problem. In Arizona, an arbitration procedure has been enacted to negotiate the amount of the billing. Surprise billings with your kind of coverage are unusual. One possibility would be if your billing provider did not accept Medicare assignment.

Yes make sure you give the insurer a chance to correct any errors before you approach your doctor. Some doctor’s have a point person who understand the complexities of how your insurer works and can help. They also have social workers who can often help.

Also I would find a trustworthy a “certified counselor” (like Donald of Arizona) who knows the ins and outs. It’s almost too much intellectual effort to try to figure it all out on one’s own.

The main thing here is that the procedure was a success and you already feel better. Like your president Trump would say: “It is what it is”, I sure hope he doesn’t run for a second term and the next administration can do decent work when it comes to medicare. In Canada, receiving a bill like this would be totally unconceivable.

Obviously, you hit a nerve by all the e-mails you received. This is why we didn’t need another conservative judge on the Supreme Court who may strike down Obama Care which has saved lives.

Jon, what a shock to receive that! However, no matter how grateful you feel for how you now feel from the procedure, you must be an advocate for yourself. I would follow what Julie and Charlotte Estep suggested. Call medical records and get a detailed itemized list of charges. Look them over carefully. (My 71 year old mother was charged for a circumcision, and for oral medication, when she was not getting anything by mouth or feeding tube). Then, wait. Your credit won’t get dinged. Sometimes it takes a few months for Medicare and your supplemental insurance to catch up. I would not have the hospital double check things-in whose interest would that be?

Good luck with all this. I know looking over these bills can be mind boggling. You’ve been an advocate for your body, now you must be one for your finances!